I hope spring is finding you well. Providing a clear-eyed look at the real story of real estate in the Roaring Fork Valley — moving past the headlines and the noise — is a pillar of my business, and this month I have something I'm especially excited to bring you.

For the first time, Compass Chief Economist Mike Simonsen built a dedicated data set for Compass Resort, the national second home and resort agent group I founded a few years ago. It's the first research of its kind for Compass, and for a market like ours that has always operated by its own rules, it's a genuine milestone. I'm proud to share it here.

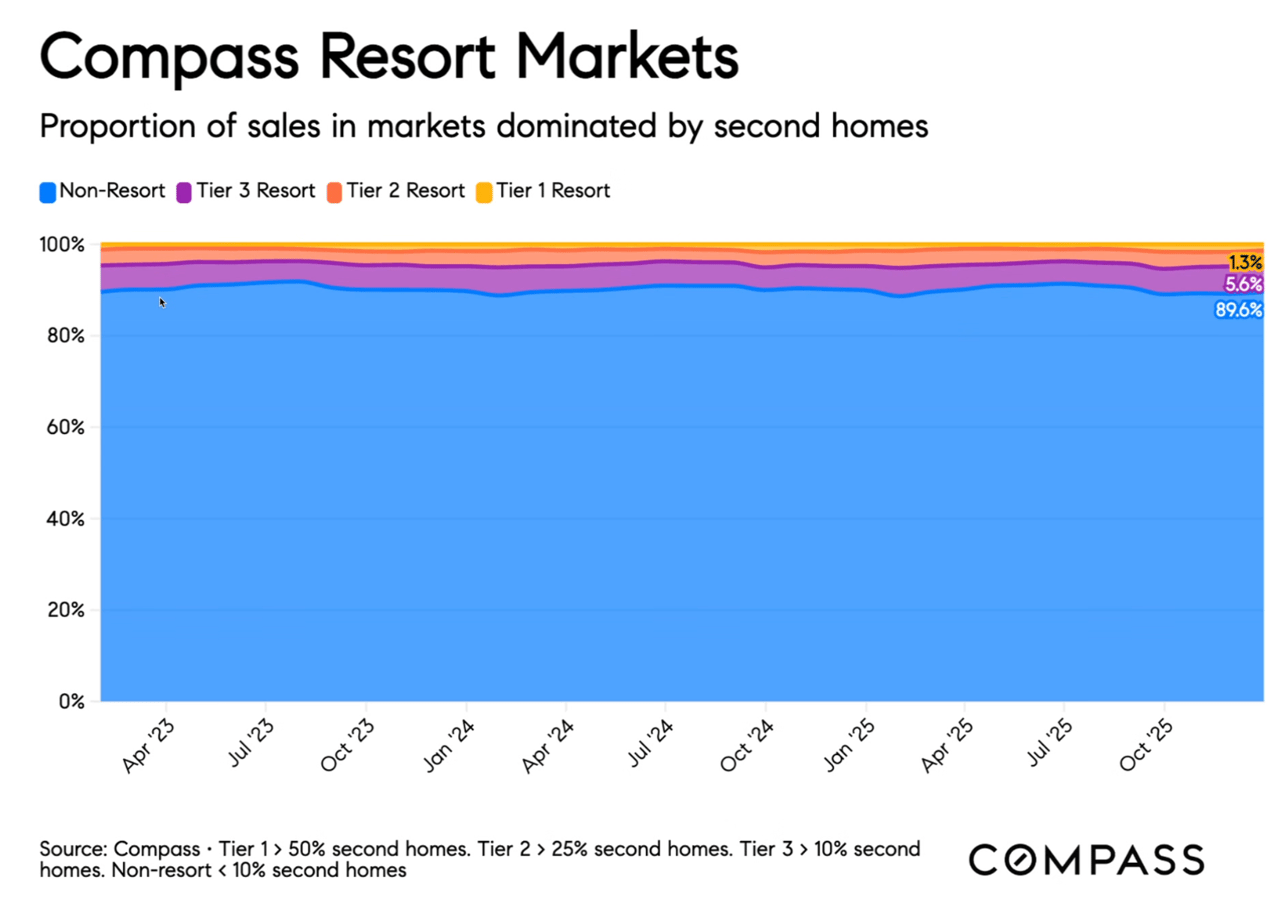

The real story is a shift from reactive urgency to high-conviction intention, as well-capitalized buyers look past short-term equity volatility to anchor their wealth in the Roaring Fork Valley. While national real estate headlines focus on the "89.6%", our Tier 1 (more than 50% second-homes) market continues to operate by its own rules—rewarding those who prioritize long-term legacy over temporary market noise.

01 · Who's actually buying right now

An estimated $6 trillion was passed down globally in 2025 alone, creating a new wave of well-capitalized buyers moving quickly and often paying cash. These buyers are weighting real estate more heavily in their portfolios than older generations — treating it as a long-term store of value and a legacy asset, not a speculative purchase. The next wave of buyers in this valley is younger, intentional, and well-resourced.

02 · Resort markets are a different universe

The national narrative is describing 89.6% of the market — not this one. When you read a national housing headline about rising inventory, price reductions, or buyer leverage, you are reading about a market that has almost nothing to do with Aspen. Tiers 1 & 2 resort markets — where between 25-50% of sales are second homes — represent just 1.3% of all U.S. real estate sales. Tiers 3 adds another 5.6%. The remaining 89.6% is what the financial press is covering. The forces shaping that market — mortgage rates, affordability, primary residence dynamics — are largely irrelevant here. Aspen and Snowmass are classified as Tier 1 — the yellow band at the top of the chart.

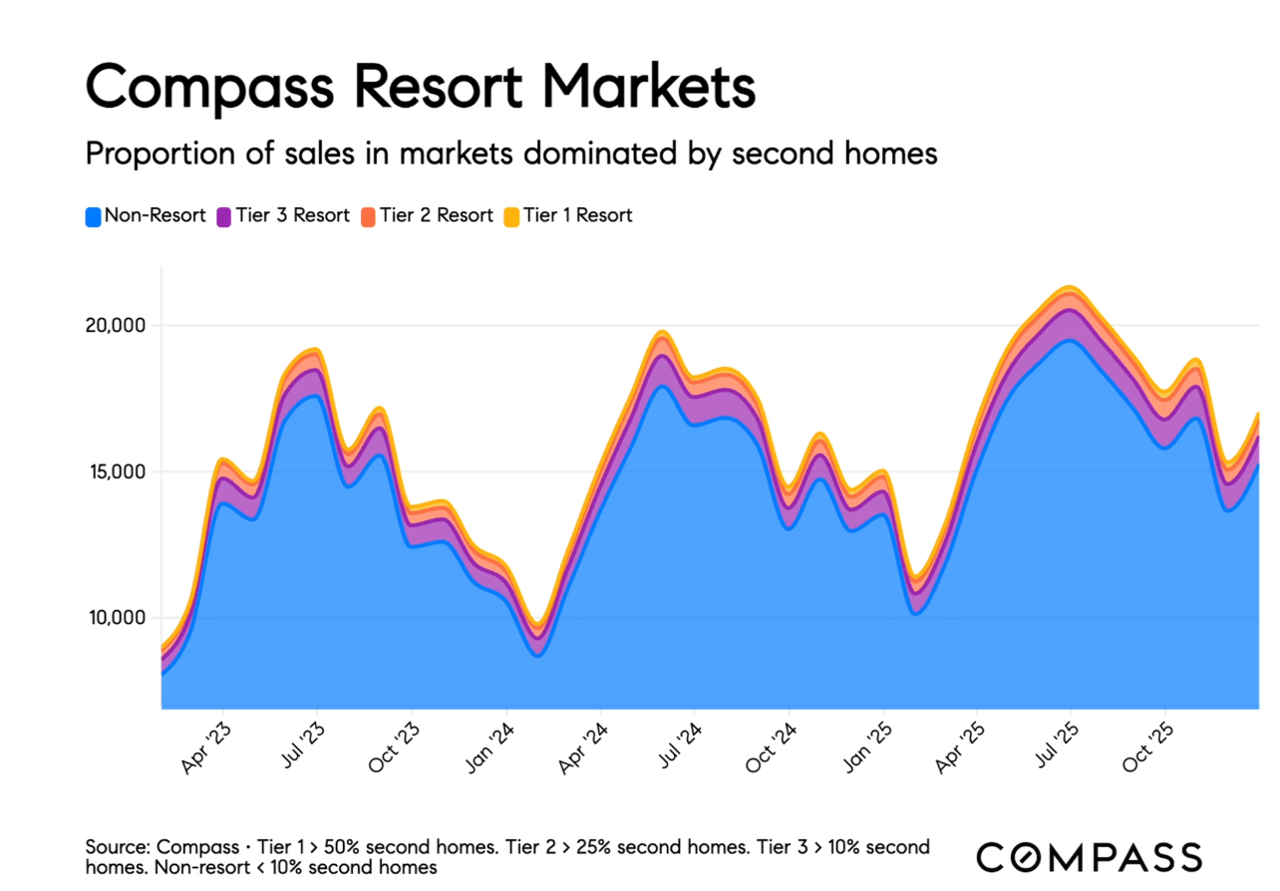

There is a common belief that resort markets are highly immune to interest rates because of cash buyers. The data below tells a more nuanced truth: even the wealthy hit the "pause" button when the cost of capital moves.Whether buyers are closing in cash, funding through a securities-backed line of credit, or carrying a traditional mortgage, the cost of capital moves in the same direction for all of them. When the 30-year fixed climbed above 7% — as it did in early 2024 and again in early 2025 — resort sales volume pulled back visibly both times. The market doesn't "break," but luxury buyers are disciplined—they often wait for the dust to settle before pulling the trigger.

03 · The wealth effect vs. the blip

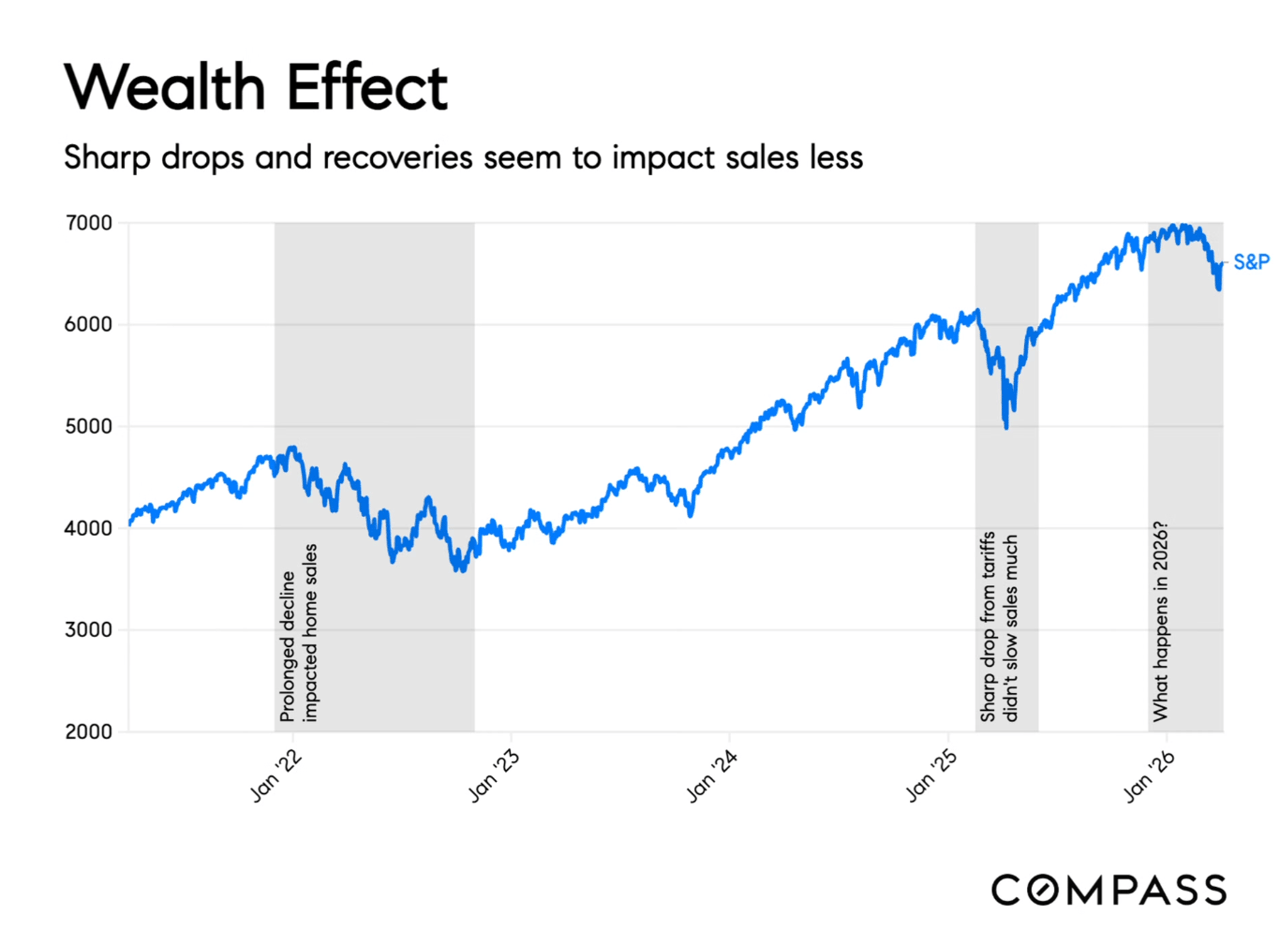

Equity markets matter more than mortgage rates in this cohort. Second-home and resort purchases are largely equity-driven; high-net-worth individuals saw their overall holdings grow by nearly 40% between 2020 and 2025. This accumulation was the primary engine behind the surge in resort demand over that period.

With equity markets showing volatility following early April’s tariff announcements, we are seeing a legitimate short-term headwind to discretionary buying at the ultra-high end. However, the pattern revealed by the data is clear: duration matters more than severity.

Sharp, short drops — even dramatic ones — have historically not translated into meaningful slowdowns in resort sales. The 2025 tariff-driven dip is a prime example: the S&P fell sharply, recovered, and luxury sales continued largely uninterrupted. This is the mechanism to watch — if volatility resolves in weeks, history says sales continue. If it stretches into months, the dynamic may shifts.

04 · Why buyers keep choosing Aspen/Snowmass over other resort markets

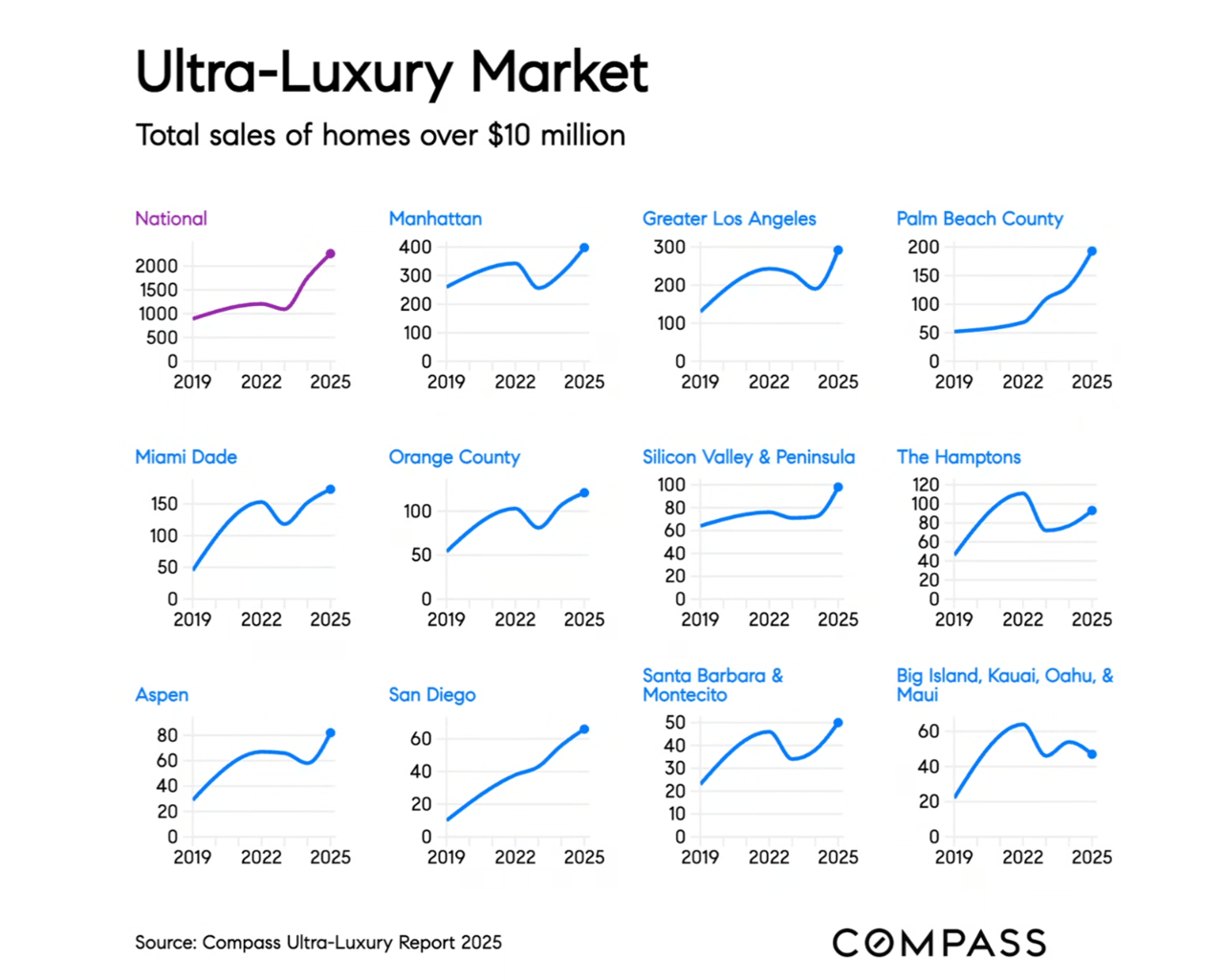

Lifestyle, privacy, and wealth preservation in a world of uncertainty. Compass's 2025 Ultra-Luxury Report found 2,261 homes sold for $10M or more nationally last year, generating $38.6 billion in sales — up 31% — with Snowmass specifically named as an emerging ultra-luxury destination. These buyers are not chasing appreciation. They are buying lifestyle, privacy, and a tangible place to anchor wealth when financial assets feel uncertain.

05 · Aspen's ultra-luxury trajectory in national context

The structural case for this market at the top end is long-term

This chart shows $10M+ sales from 2019 to 2025 across every major U.S. luxury market — and Aspen's line is one of the clearest upward trajectories on the page. From roughly 20 sales in 2019 to over 80 in 2025, the growth in Aspen's ultra-luxury segment has outpaced most comparable markets. What the chart also shows is that virtually every market pulled back in 2023 and recovered — and Aspen recovered sharply.

This isn't a "pandemic story"; it's a long-term flight toward lifestyle, privacy, and tangible wealth preservation. These buyers aren't chasing speculation — they are anchoring wealth.